First Home Buyers Part 4: Loan types and Pros and Cons of each

With the wide range of loan types out there it can sometimes seem overwhelming when deciding which is best for you. As all our individual circumstances are different it is far from the case that ‘one size fits all’.

A detailed analysis by a Mortgage Professional will assist in establishing the most appropriate type of loan for your circumstances.

This article will provide you with some basic information about the different loan types and their pros and cons.

The loan structures we’ll look at are:

- Standard Variable Rate Loans

- Basic Variable Rate Loans

- Honeymoon Loans

- Fixed Rate Loans

- Offset Accounts

- Tracker Loans

Standard Variable Rate Loans (SVR)

These loans are the top rate that lenders charge. The rate is generally discounted from the headline rate depending on loan size.

These loan types come with all the ‘bells and whistles’ and provide the flexibility allowing additional repayments, ability to redraw payments made in advance (usually at no cost), can be linked to an offset account (see Offset section) and early repayment without penalty or Break Fees.

An SVR loan would usually be taken as part of a ‘Package’ which includes an offset account, fee free or discounted credit card along with other incentives such as discounted insurance etc. Depending on the loan size the SVR rate may be discounted by up to 0.7% or more. However, many of these packages come with Annual Fees of up to $395. There are some exceptions to this and a mortgage professional like us can help to steer you through the maze.

Packages such as these are suitable for those

requiring ultimate flexibility and ease.

However, the overall cost is generally higher than basic variable rate loans unless you are likely to be holding substantial additional funds in an offset account.

Basic Variable Rate Loans (Basic)

Once upon a time these loans were indeed very basic with little flexibility, however, in recent years we have seen additional features added which make these loan types a real option. A major driver of change in this product range may have been the implementation in 2011 of new laws prohibiting early termination penalties on loans (not to be confused with Break Costs on Fixed Rate Loans).

Basic variable loans these days have almost total flexibility with unlimited additional payments allowed as well as free redraw of advance payments.

They generally come a significantly lower interest rates

and less or no ongoing fees.

However, they cannot usually be linked to an offset account and do not come with fee free credit cards and other incentives such as those offered with SVR loans and packages.

Consider these loans if you are unlikely to be holding substantial additional funds in an offset account, are happy to trade off some of the other discounts for a lower home loan rate. With the ability to redraw at no cost you are also gaining all the same interest saving benefits of an offset account without the additional cost.

Honeymoon Loans

To be blunt, these loan types offer little advantage. They come with a discounted rate (usually fixed) for the first period of 1 – 3 years depending on the lender BUT after that period the rate goes up substantially. Unless you need that repayment relief for the first 1 – 3 years you are better off looking at the other options.

Fixed Rate Loans

Fixed rate loans offer a period of 1 – 10 years where the rate and loan payments will not change. They are usually restrictive in that they have limited or no ability for additional repayments, no redraw (for those that do allow some extra payments) and no ability to link to an offset account.

There are a few lenders that do offer offset accounts

or redraw with fixed rate loans so these are worth consideration

if you are looking at a fixed

rate option.

If you decide to sell your property or otherwise pay-out your loan during the fixed rate period you may have to pay substantial Break Costs. This is a complicated calculation but is essentially the amount the bank loses through you breaking the fixed rate contract.

On the positive side, Fixed Rate Loans offer security of repayments in that you know exactly what your weekly, fortnightly or monthly commitment will be for the period you have fixed your loan. It’s often not the case of ‘winning or losing’ but rather that assurance that the payments that you are comfortable with won’t be changing during that period.

When a fixed rate loan expires, you have the option of fixing again for another period at the rates current at that time or allowing the loan to revert to the current variable rate on offer.

Note: There are a small number of lenders that offer more flexible fixed rate loans. Some allow additional repayments and redraw while others allow an offset account. However, beware of any offset account that is not 100% offset.

Fixed rate loans are suitable for those who are concerned about the impact of rising interest rates and would like the stability of set repayments.

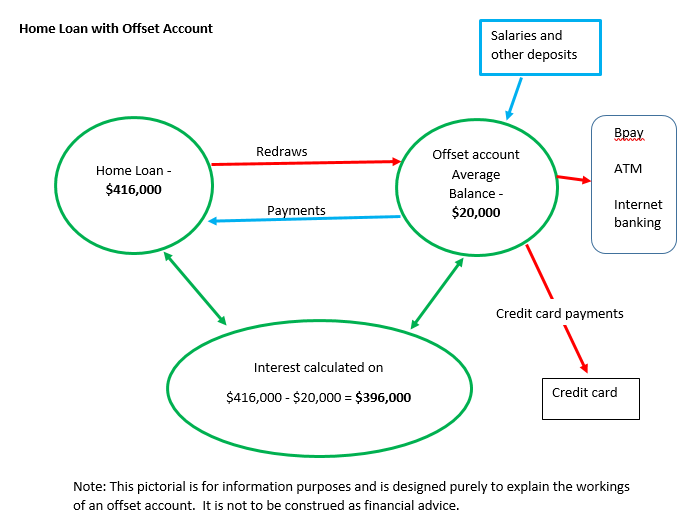

Offset Accounts

These are not loans but they are attached to certain types of loans (as referred to above) as a mechanism of saving interest. An Offset Account is a standard transaction account that is linked to your home loan and as the name implies, any funds held in the offset account reduce the interest paid on the loan by netting the balances off against each other.

The graphic below best describes how these work.

In this example, the borrower is ‘saving’ interest on $20,000 at the same rate as the loan which is substantially more than the interest they would ‘earn’ in a savings account. AND the ‘saved’ interest does not attract a tax liability.

Some people maximise the amount they hold in their offset account by paying all their expanses, shopping, groceries etc. on their credit card and, utilising the interest free period on the card, sweep the card back to zero on the last day hence incurring no credit card interest.

A word of caution though. While effective, this method of maximising your interest savings requires total dedication and a disciplined approach. If you rack up too much on the card to enable you to pay it all back down, you’ll not only undo the benefits of the offset account but will most likely end up worse off due to the high interest rates on the credit cards.

Also, make sure that your offset is a 100% Offset account. Some lenders only apply a 40% offset with certain accounts.

Tracker Loans

These are brand new to the Australian market and at his stage only offered by a very small number of lenders.

With the Australian Securities and Investments Commission (ASIC)

pushing for more of these products it is likely we’ll see

an increase in the number of lenders

offering these loans in the

coming months.

How They Work

Typically linked to the Reserve Bank of Australia’s (RBA) Cash Rate the lender applies a fixed margin to that rate and this is what the borrower pays. Any movements in the RBA’s Cash Rate (announced on the first Tuesday every month except January) are automatically reflected in the rate you pay. Furthermore; your new rate is generally applied within a couple of days so you get the benefit of any reductions almost straight away. The following is an example of how it works.

The current cash rate is 1.5%. Let’s say the lender applies a fixed margin of 2.4% to that rate so you’d be paying 3.9% (1.5% + 2.4%). Now let’s say that the RBA cash rate reduces by 0.25% to 1.25%. The bank’s margin of 2.4% is locked in so your rate automatically reduces to 3.65% and almost straight away.

Conversely, if the cash rate increased by 0.25% your rate would become 4.15%.

The advantage of these loan types is that you have certainty over the degree of increase or decrease in your interest rate. No more ‘out of cycle’ rate changes and no more of the bank holding back rate reductions and increasing rates more than the RBA increase.

To book an appointment, find out more information, or to receive a FREE copy of our First Home Buyers’ Guide, please register your interest below.